In

GAB The Story, I ended with the remark

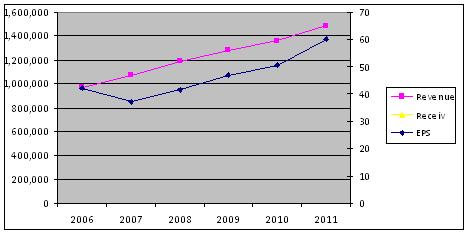

steady growth but nothing explosive. To illustrate this statement, I charted out the

EPS(Earnings per share) and

Revenue of GAB from 2006-2011. FYI, financial year end for GAB is 30-June.

So preditable that I can almost draw a straight line into future projection. Notice how the 2008 global financial crisis didn't hamper earnings.

Profit margin at 31% is decent. Carlsberg is at 30-ish% as well.

Operating expenses for

SGA (Selling, general & administrative) rose 30% from previous year. At 49% of gross profit, SGA expense is still very alright. Just gotta keep an eye on the yearly increment.

GAB does not need to incur much spending on

CAPEX (Capital expenditure). 31 million in 2011, which translate to 17.5% of net earnings. Depreciation is corresspondingly low.

GAB has a

cash pile of 178 million and

ZERO borrowings.

Due to its zero borrowings, I will not go into gearing ratios. Cos they will be err, zilch.

So, is GAB a cash cow? Lets look at its

FCF (free cash flow). Free cash flow is Operating cash flow minus capex. FCF yield in 2011 is 5.36%, an increase of 40% from previous year. Nice.

ROE (Return on Equity) in 2011 is 35%, compared to peer Carlsberg 23% (FY 2010). Take caution when reading into this ratio, as it is affected by the debt level. Highly geared companies can have higher ROE. ROE is meaningful here as GAB has zero gearing.

So far, GAB looks pretty awesome doesn't it? It is obviously a solid and financially sound company. I'd love to own shares of it. But the big question,

what is the right price to pay? I should be buying at fair value, or even better, when it is undervalued.

Let's dive into price ratios.

The most popular of all ratios,

PE (Price over Earnings) Ratio.

On 22 Nov 2011, PE ratio of GAB is

17.69.

There is only 1 other comparable listed brewery, Carlsberg. PE of 16.67

Growth rate of GAB over 5 years is

7.19%PEG (PE over growth) ratio is therefore

2.46.

More on PEG, read my previous post

PEG RatioAt the current price of RM10+, GAB is rather overpriced, in my opinion.

What is the

fair price for GAB? I use

Discounted Cash Flow (DCF) model. But seriously, don't rely too much on it as it has many variables. You know what they say, garbage in, garbage out. I adjust the calculations such as discount factor to my own comfort level. And I am conservative. Throw in all the numbers, and DCF regurgitates

RM7.80. That is my number.

There is an excellent tutorial on DCF calculation on Investopedia. Comes with example to guide you through the whole process. If that's too much trouble, there are DCF calculators (usually in spreadsheets) that you can download from the Net.

In summary, I'd

buy GAB for the long term, but not at this price. I'm anticipating a recession. Read

Macro Outlook 15-Nov-2011. My chance will come.